Automate your fnf settlement with a robust software solution that enhances efficiency and accuracy in the final reconciliation process.

The full and final settlement is a process of the clearance of dues that have been earned by an exiting employee during their term of service from the resignation letter date to their last working date. Irrespective of the type of exit – voluntary resignation, retirement, or termination. The company is liable to release different payable dues of their salaried employees after their exit.

It is an essential stride in the HR workflow to evaluate and remunerate employees’ dues after their exit from the organization as it results in satisfied employees and enhances the company’s internal and external image.

After an employee resigns, from that particular day till their term in the company ends is considered as the ‘notice period‘ of the employee. When the employee accomplishes the notice period term with the proper handover of documents, assets, and knowledge acquired during their term of service along with no contractual obligation, they are entitled to receive the full and final settlement clearance from their company.

The full and final settlement (fnf) has multiple benefits for the employer, employee, and the organization. It has an inevitable significance that shapes the organization’s image. Let us contemplate it in detail:

The full and final settlement process involves multiple steps to attain clearance from numerous departments.

A company is composed of diverse departments and when an employee decides to exit, they have to get clearance from the concerned departments to get their full and final dues.

The departments responsible for making clearances generally include IT, administration, HR, and finance departments.

The IT department is responsible to collect all the official gadgets and login IDs that were provided to the employee for the duration of their service.

Recovery of company assets includes mobile phones, laptops, and other gadgets provided to the employee during the term of their employment.

The department should ensure the gadgets are robust and there are no damages. Besides, access to all official logins is blocked.

In case of non-recoveries, the IT team can stop the FnF processing and in case of damages, it can recover the damaged amount from FnF.

The Administration department is liable to collect the identity cards or other access required for the entry and exit of the employee.

The admin head is the responsible person who verifies the entire process of recovery and has the authority to let up the processing of full and final settlement payment until recovery.

The Finance team is accountable to process all the balance payments in the FnF settlement process after making necessary deductions and additions (if any).

Various components are taken into consideration while calculating the FnF like the outstanding expenses, expenses on the company’s card, additional expenses incurred, and others.

After the notice period is duly served by the employee, The HR team signs the last document confirming the handover of all assets and clearance from all the departments.

The HR department has the final job of processing the FnF settlement.

The 5 essential documents that are necessary during the full and final settlement are:

The first and foremost document that is needed for full and final settlement is the resignation letter of the employee. There should be a formal resignation letter submitted to the employer by the employee mentioning the last working day, reason for exit, and commitment to hand over the company’s assets and knowledge before leaving.

no dues certificate is a document indicating that the exiting employee or employees have cleared all their dues with various departments like finance, IT, HR, and administration. Diversion to which shall withhold their no dues certificate resulting in the delay of fnf settlement.

A comprehensive report on unused paid leave is required to pay the leave encashment dues, further, the attendance of the employee is evaluated to calculate the number of working days attended by the employee during the period of notice. Any leaves availed during the notice period are subject to deductions, etc.

A return checklist form of all the assets and accesses that in in possession of the exiting employee. The list is thoroughly checked to ensure that all the company assets such as laptops, phones, etc are operational and are duly returned by the employee. Further, the login access of the employee is revoked.

A final finance calculation sheet depicting the breakup of the final settlement amount which includes salaries, deductions, bonuses, compensations, benefits and leave encashment, etc.

Multiple major components are taken into consideration in evaluating the FnF, namely:

1. Unpaid Salary

2. Additional Earnings:

3. Accumulated Interest

4. Gratuity Payment

5. Deductions including:

Unpaid salary is the outstanding wages of employees that are not paid on time during their employment. Salary earned in the month of notice or any salary due from the preceding month of employment is considered unpaid salary.

According to The Payment of Wages Act 1936, employees are entitled to receive their salary on time for their term of employment, and if the company or employer refuses or fails to pay the amount, the employer is liable to pay an interest amount along with the due salary.

The number of days of compensation is multiplied by the gross salary divided by the average number of working days in a month.

✱ The No. of Days of Compensation x Gross Salary/ 26 (Avg. working days in a month) = Unpaid Salary.

It includes various allowances and bonuses provided apart from the basic employee’s salary during his term of service like:

Apart from casual leaves, employees are also entitled to privileged leaves (PL). If PL has not been availed by the employee during their tenure, leave encashment is paid during their exit and is added to the full and final payment.

The leave encashment of privileged leaves varies as per the company policy and norms. It is never the same for all companies as every company’s policy is different.

In addition, employers provide bonuses to employees on special occasions (e.g. Diwali Bonus), statutory bonuses, or due to their meritorious performances and significant contribution in their job role. The cash equivalent to the bonuses is added to the full and final settlement payment during the exit of the employee.

As mentioned, PL for leave encashment varies as per the company policy, so approximately,

If the PL is considered 21 Calendar days a year, the calculation will be:

✱ (Basic Salary + D.A.) / 30 (No. of working days to be enchased).

If Pl is considered 21 working days a year, then the calculation changes to:

✱ (Basic Salary + D.D) / 26 (No. of working days to be enchased).

A statutory bonus is an annual or monthly incentive given to an employee whose income is less than 21,000 a month. The Payment of Bonus Act, of 1965 provides a minimum bonus of 8.33 percent and maximum annual benefits of 20 percent of wages to the employees.

The Act applies to all establishments with more than 20 employees. Some companies choose to pay this out in advance. The calculation is undertaken using the formula:

✱ Statutory bonus = Salary (Basic + DA) * Bonus Percentage

These are the termination payments undertaken by the company to the employees during a layover.

The reason for employee termination could be numerous, ranging from non-requirement of personnel for a particular job role to termination due to liquidation of the company, or any other reason.

An employee is eligible for this payment only when they have completed 2 years of service in that particular company.

✱ Employee aged of more than or equal to 41 years = 1 and half weeks pay for each full year

✱ Employee aged more than 22 and less than 41 = 1 week pay for each full year

✱ Employee aged under 22 =half a week’s pay for each full year.

These are the unpaid and accrued interest that has not been paid over the duration of time.

The Payment of Gratuity Act of 1972 has laid certain rules for the payment of gratuity amounts. It is paid to employees who have completed 5 years of continuous term in an organization without any gap in between.

The company is liable to pay the gratuity amount within 30 days of the employee’s exit. By law, the government has made it mandatory for organizations to pay gratuity within 30 days of an employee’s exit else a simple interest is required to be paid from the due date till the date of payment by the employer.

Most companies deduct 4.81% from the employee salary and pay it during the exit of an employee as the gratuity amount.

As the gratuity paid to employees is a part of their salaries, it is eligible for income tax deductions. However, it is subject to limited deductions due to various exemptions laid by the government.

If the company policy is covered under Gratuity Act:

✱ Gratuity = n*b*15 / 26

If the company policy is not covered under Gratuity Act:

✱ Gratuity = n*b*15 / 30

Any tax liability that is eligible for income tax is deducted from the full and final settlement payment.

In accordance with the Income Tax Act, of 1962 a TDS (Tax Deducted at Source) is deducted from the components that are qualified for taxation.

Deductions include Provident Fund, ESI (if applicable), Employee’s Income Tax, etc. However, gratuity and leave encashments are exempted from TDS.

Provident funds are the invested funds made out of partial payment from both the employer and employee for long-term savings to back up the employee’s retirement.

Most confuse provident funds with pension benefits. A provident fund is the combination of the employer’s and employee’s contributions for retirement benefits whereas, a pension fund is the employee’s contribution for retirement purposes.

Pension funds are eligible for withdrawal when an employee completes 10 years of continuous service. So, it is important for the employee to obtain the EPS certificate and hand it over to the new employer to maintain continuity of employment.

Under the Employee Pension scheme, the minimum Pension amount is ₹ 1000 to ₹ 2000 per month for India.

The employee has to contribute 12 % of (basic salary + DA) towards the PF contribution.

The PF percent varies from 10-12 % for employees and 12% for the employer.

From the employer’s contribution, 8.33% is shared towards an employee’s pension scheme and 3.67% is shared towards the EPF scheme.

✱ Employee’s monthly salary = (pensionable salary * pensionable service) / 70

ESIC benefit deductions are applicable for employees whose monthly salary is less than ₹ 21,000.

The ESIC Act, of 1948 has fixed a percentage of contribution for both employer and employee.

The ESIC rate is revised from time to time. Currently, the employer contribution for ESIC is 3.5% of the salary and the employee’s contribution is 0.75%.

✱ The calculation of ESIC is done on the basis of 26 days and not calendar month.

This is the amount deducted from the gross salary of the employee in case of advances drawn from the company in any preceding month.

The Full and Final settlement calculation process includes the deduction of such an amount from the employee during his exit.

✱ Total gross salary (including all earnings) – advances received.

It is extremely vital for the employer to process the final settlement as it has an advantageous output for both the employer and the organization.

The benefits might be indirect but are prolong and vivid. Various benefits of clearing FnF include:

Employee satisfaction reflects the work environment’s culture and how the workforce is treated.

A smooth and quick final settlement process not only enhances the reputation of the company but also boosts the morale of the internal employees.

It showcases the strong work culture and positive work environment of the establishment.

When an employee leaves a company with hassle-free exit procedures and a streamlined FnF process, it creates an optimistic experience which, as a result, enhances the organization’s reputation.

It is a basic human tendency to discuss previous companies’ pros and cons with the current ones. As a result, the staff tend to discuss the quick and streamlined FnF settlement procedures with others which not only magnify the employer’s image but also attract the finest candidates to associate with the organization.

The financial year (i.e. 1st April to 31st March) auditing to evaluate the company property, assets, and liabilities are conducted every year to keep a watch on the processing and functioning of the organization.

Accumulating the FnF amount of employees ultimately affects the functioning of the organization during the audit. It puts the company’s evaluation in trouble and degrades the credibility of the company. In contrast, when the full and final settlement is streamlined, it smoothens the audit process and frames a clear picture of the flow of investments and expenses incurred.

In India, there are no specific regulations for undertaking the Full and Final Settlement (FnF). Every company has its policy and rules for the FnF process.

However, according to the Payment of Wages Act 1935, an employee is entitled to payment according to their terms of service.

There are certain state laws like the Commercial Establishment Act, Wage Code, New Wage Code, Labour Law, and more, that can be referred to during the FnF process.

Ideally, the maximum duration for making a full and final settlement is 30-45 days after the last working day of the employee. The day when the notice period ends is considered the last working day.

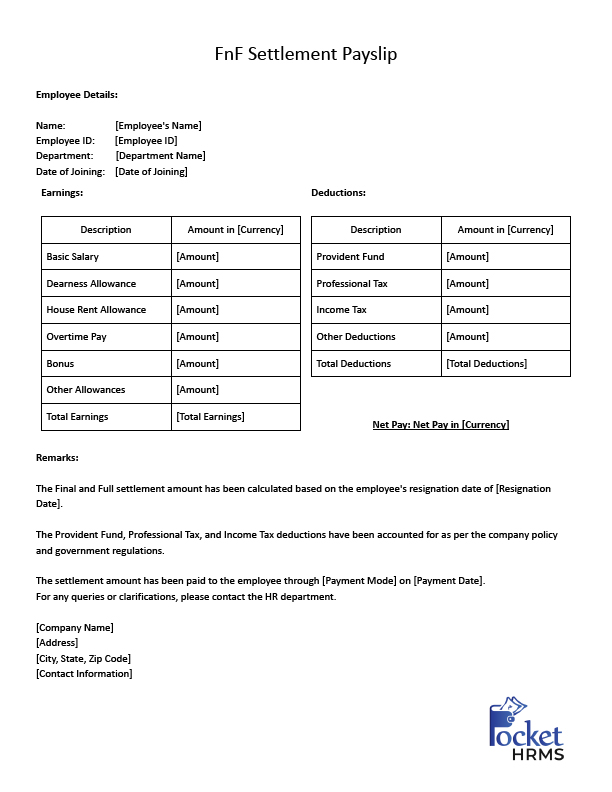

The FnF settlement format for payslip does not have any specific format to be uniformly followed by all the establishments.

The basic full and final settlement payslip includes the following details:

after understanding the f&f meaning, let us understand the process of full and final settlement has the following steps:

Accepting the employee’s resignation is the first step of the full and final settlement process in which the company should accept the request of the employee to leave the organization.

Giving a response to the resignation showcases the ideal conduct of management towards human resources.

After receiving the resignation letter from the employee, the employer sends an acceptance letter to acknowledge the exit date and process the final settlement accordingly.

Next in the queue is the handover of all official gadgets and access provided to the employee during their term of employment.

The employee is expected to return the asset intact and the login access maintaining the confidentiality policies of the establishment.

Different departments like IT, HR, Finance, and Admin provide clearance after verifying the returnable from the employee.

It ensures zero data theft and maintains the credibility and confidentiality of the company.

After getting clearances from different departments, the full and final settlement is processed and released within 30-45 days of the employee’s exit after serving the notice period.

Later, the experience certificate is also provided to the employee for investing their knowledge and skills in the company.

It enhances the employer’s reputation for both existing as well as exiting employees.

The FnF settlement procedure is a tedious process for the payroll team specifically since its evaluation of adding the cash benefit, calculating the face salary deductions, and more. Automation in the FnF settlement procedure not only quickens the process but also eases the task and benefits in managing time better. FnF is calculated on the regular salary schedule and a streamlined FnF procedure exemplifies the vigorous and supportive management team. After getting an insight into the f&f meaning, fnf full form and its significance, you should select the best HRMS that will be a boon to your HR’s processes and will enhance the efficiency of the full and final settlement process to optimum.

The f&f full form is full and final settlement. It refers to the process to clear the dues of employees which includes their salaries. unused paid leave encashments, bonuses, compensations, deductions, etc.

The timing of full and final settlement (fnf) varies as per different company policies, employment contracts, labor laws obligations, etc. However, it has generally been processed after the last working day of the employee. The essentiality of the full and final settlement letter is to ensure that all the financial dues and obligations between the employer and employees are fairly resolved.

The full and final settlement time period is the time within which the employer is liable to clear the dues and obligations of the exiting employees. Although there is no specific time mentioned in the Payment of Wages Act 1936, as per experts, the ideal time period to complete fnf should be somewhere between 30-45 days after the employee’s last working day. Some organizations take 90 days after the last working day of the employee for fnf settlements.

However, as per the Payment of Wages Act 1936, in case of termination of employees, the employer has to clear the fnf within 2 working days after termination. As per the Factories Act, of 1948, the used leave encashments and bonuses must be cleared by the 7th or 10th of the following month after the resignation of the exiting employee.

If the employer fails to pay the full and final settlement even after fair compliance with exit rules by the employee, then the employee can sue the organization in a court of law and can also approach the labor commission. If the employee is avoided after the exit and the employer intentionally stops the process of fnf then the employee can lodge a complaint to police against the employer.

Under the New Wage Code, employers are required to clear the fnf settlement within 2 days of employee’s last working days. Earlier it was settled within 30-45 days or 90 days of employee’s last working days, but now the new laws have mandated companies to pay the fnf within 2 days of employees exit.

Yes, gratuity is included in the full and final settlement. It is a major component that is evaluated in the process of fnf. Under the Payment of Gratuity Act, of 1972, Gratuity is paid to employees who have completed 5 years of continuous term in an organization without any gap in between. Most companies deduct 4.81% from the employee’s salary and pay it during the exit of an employee as the gratuity amount.

The HRMS software can ease your fnf settlement in multiple ways such as:

The HRMS software automates the offboarding process by accelerating the exiting formalities and tasks. The quickening of the process facilitates the employers’ ease in calculating the fnf settlement conveniently with efficient reports and analytics.

The best part of HR software is it automates the evaluation of the fnf components hence eliminating the scope of manual errors. It provides error free reports that is reliable for further processing and dues clearance of employees.

The HRMS software collaborates with other systems such as attendance management system (GPS attendance system, biometric attendance system) leave management system, and payroll software to extract accurate data such as the total number of leaves taken by the exiting employee from the date of resignation to the last working day, exact location and time of clock in and clock out from the work location, etc, that are required for the evaluation of fnf. This as a result helps in the extraction of credible and error-free fnf reports.

It helps to comply with the labor laws that state clearance of all dues of exiting employees within 2 days of the last working day. It can be achieved only by the company which has automated fnf management that streamlines the offboarding tasks and fastens the process.

The HRMS payroll software notifies the full and final settlement dates and alerts the employer to process the dues within the time frame hence facilitating compliance within the time frame and strengthening the image of the company in the market. The ESS portal (Employee self-service portal) of employees enables them to view any clearances or handover due from the employee before their exit, hence notifying them about the clearances before they leave. This proactive approach helps eliminate potential issues and delays in the FnF process after the employee has left the company.

Yes, taxes are deducted from the full and final settlement amount. However, specific deductions depend on various factors, including the nature of the payments made in the settlement, the employee’s salary structure, and the applicable tax laws in the country, etc. Various components of fnf settlement like Provident Fund, ESI (if applicable), Employee’s Income Tax, etc. are taxable whereas gratuity and leave encashments are exempted from TDS.

Yes, a full and final settlement is mandatory for all the employees who comply with the company’s exit policies and cooperate in making the transition happen with ease. Irrespective of the type of exit by resignation, termination, etc. employees have the right to get their dues cleared with the organization, subject to the condition they adhere to the policies, obligations, and exit formalities duly.