The best credit card processing companies are secure, easy to use, and offer transparent, competitive pricing.

Senior Staff WriterTechnologyAdvice is able to offer our services for free because some vendors may pay us for web traffic or other sales opportunities. Our mission is to help technology buyers make better purchasing decisions, so we provide you with information for all vendors — even those that don’t pay us.

Published Date: July 24, 2024Table of contents

We then hand-picked seven credit card payment processors based on our custom evaluation methodology, which evaluated 28 data points across six categories: Price, Hardware, Features, Support and Reliability, User Experience, and User Scores. Ultimately, the best options stood out for impressive functionality, quality support, and best value for money.

Over the years, technology has made it possible for customers to use credit cards in person and online in a variety of ways. As a result, credit cards are one of the most popular payment methods today because of the convenience they offer.

The challenge for businesses is choosing the right credit card processor that is convenient for customers, easy to maintain, and offers low, competitive pricing that won’t cut into their profit margins.

Based on our evaluation, the best credit card processing companies for 2024 are:

Helcim

Interchange plus $15 (refundable)

Payment Depot

Interchange plus By request

PaymentCloud

By request

Stax

Wholesale subscription Volume-based plansSquare

Waived up to $250/mo. By request

CardX

Not disclosed Volume-based plansCDGCommerce

$25 (refundable) Volume-based plansExpert Tip Surcharging is when businesses pass credit card processing fees on to customers by including an extra fee in the transaction. This practice is gaining popularity among merchants and is increasingly supported by payment processors. While it is possible to impose surcharging by manually adding fees, the easiest and most compliant way to minimize processing fees with surcharging is by using a processor that automates the process.

Why we chose Helcim

Helcim is our overall top choice for credit card payment processor. Helcim is a traditional merchant services provider, meaning each business has a dedicated merchant account, which offers maximum stability.

Yet, for a traditional merchant account services provider, Helcim is among the easiest to set up, use, and scale with a business. All of its credit card processing services are accessible without a monthly fee.

We love how Helcim built its software around automation. Helcim’s pricing structure provides interchange plus rates with built-in automated volume discounts. And, unlike other payment processors, every merchant account is automatically qualified for the in-person and online zero-cost processing program. Helcim even automatically gathers the additional information required for B2B businesses to qualify for level 2 and 3 discounted rates.

One of Helcim’s stand out features is its automated volume discount pricing. Helcim has structured its fees so that discounted rates are built-in based on the average sales volume for a period of three months. With this, businesses don’t have to send a request or subscribe to a higher monthly plan in order to reduce transaction rates.

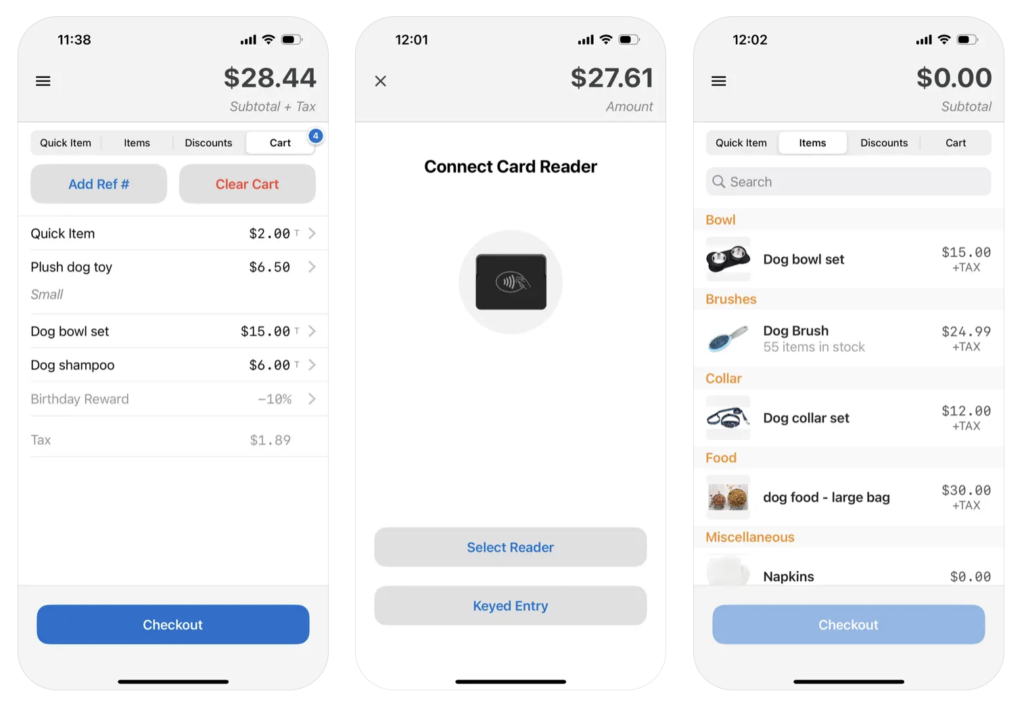

Helcim can process in-person and online credit card payments. It comes with free invoicing, subscription management, virtual terminal, online checkout, and POS platforms. Helcim does not charge a markup for accepting foreign credit cards and automatically qualifies its merchants for free credit card processing via surcharging and level 2 and 3 data processing for B2Bs.

Helcim also provides business tools for payment processing at no additional monthly cost. The CRM is fully integrated into the POS app, online checkout, and virtual terminal. The inventory feature in the POS app is synced with your ecommerce website. A secure card vault is also available to store customer payment information for recurring transactions.

Helcim’s free credit card processing feature is fully automated. Businesses do not need to apply separately to access this feature, which can be activated and deactivated for every translation with a simple toggle option. Once you decide to apply this feature, Helcim automatically detects which method is best to use based on the customer’s location and mode of payment.

Overall Reviewer Score

Average User Review Scores

Why we chose Payment Depot

Payment Depot is a traditional merchant account service provider that was acquired by Stax (formerly Fattmerchant) in 2021. It provides credit card and other non-cash payment processing tools for all business types and sizes, supported by Stax’s secure platform.

Early this year, Payment Depot’s pricing structure changed from wholesale subscription (similar to that of Stax) to custom interchange plus pricing. This move allowed Payment Depot to distinguish itself from Stax by providing a more sustainable pricing approach to mid-size businesses that are interested in Stax but do not want the high monthly fees.

Payment Depot can process a wide range of credit card services. It works with Swipe Simple to provide a mobile POS app that connects with a Swipe Simple mobile card reader to accept swipe, EMV, and contactless payments. It can also accept credit card transactions online.

Payment Depot users will have access to payment processing services available in Stax. These include invoicing and recurring billing tools, cross-border transactions, level 2 and 3 data processing, a secure card vault, and a virtual terminal for processing manual payments.

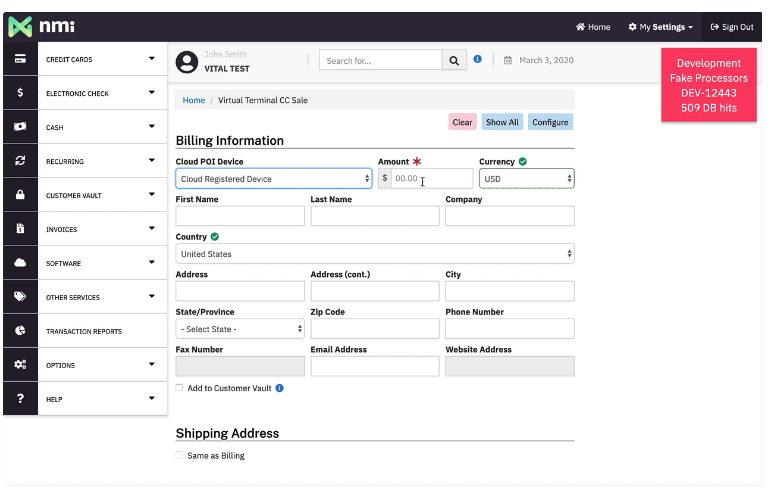

Payment Depot works with a number of payment gateways. This includes the popular Authorize.net, Network Merchants Inc. (NMI), and PayTrace for B2Bs that want to accept level 2 and 3 discounted rates. Payment Depot’s gateways can easily be integrated with well-known ecommerce platforms like Shopify.

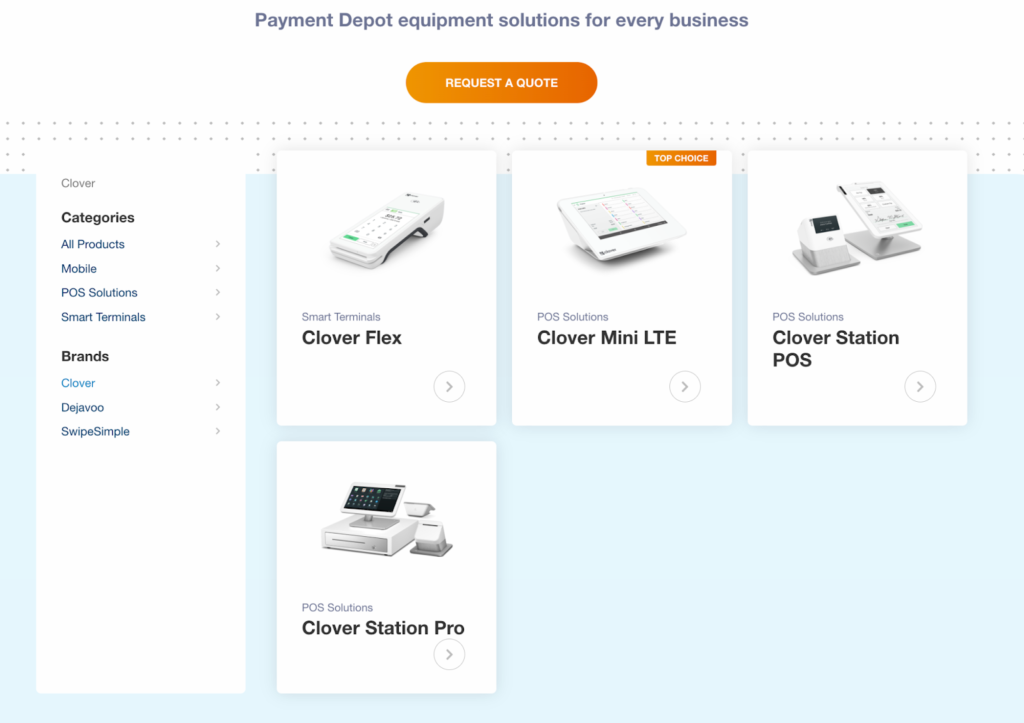

Payment Depot is compatible with a number of POS hardware and card terminals. You can use Payment Depot’s credit card processing service along with Clover’s suite of POS hardware. Swipe Simple’s mobile card reader and mobile POS app are popular choices. Dejavoo card terminals are available for those who need smart, stand-alone systems.

Overall Reviewer Score

Average User Review Scores

Why we chose PaymentCloud

PaymentCloud is a traditional merchant services provider for all business types, but it is well known for its high-risk merchant expertise. Even other popular payment processors work with PaymentCloud to provide hard-to-place businesses with a merchant account. It claims a 98% high-risk account approval rate and approval time as fast as 24–48 hours.

With its services built on customization, PaymentCloud offers the most scalability of all high-risk credit card payment processors. Aside from providing an entirely customized payment services solution, it can adapt its fees based on the client’s preferred pricing structure and seamlessly integrate with any payment gateway so clients can keep using what it already has in place.

The system is also compatible with a variety of POS hardware, like Clover.

PaymentCloud supports both in-person and remote credit card payment methods. Users can accept mobile payments with wireless card terminals for swiped, EMV, and contactless transactions, including QR code scan to pay. It can also be used to accept credit cards and other non-cash payments online, like ACH and cryptocurrency.

PaymentCloud offers a full set of payment processing tools, such as invoicing, recurring billing, and manual payments via a virtual terminal. It also supports cross-border transactions, B2B, surcharging, and multicurrency tools that most high-risk businesses need. PaymentCloud is gateway-agnostic, which means merchants can keep using their current payment gateway or seamlessly migrate to a different platform that can better support their business payment processing needs.

PaymentCloud is well-known for its hands-on approach to client onboarding. It assigns a dedicated account manager who will assist businesses throughout the application process, providing cost analysis and assessing payment processing requirements.

Chargeback management is a key factor in sustaining a high-risk merchant account. Every PaymentCloud credit card processing service is equipped with high-level data encryption, 3D secure technology, and a variety of fraud detection tools such as address verification and the ability to pause suspicious transactions.

Overall Reviewer Score

Average User Review Scores

Why we chose Stax

Stax is our most recommended credit card processing company for established businesses.

Over the years, it has acquired several companies, such as Payment Depot and CardX (formerly Fuse Bill), to build its portfolio of payment processing services for different industries and business types. Stax’s subscription-based pricing (wholesale interchange rates with low per-transaction markup) and unlimited payment software access provide high-volume businesses with the best value for their investment.

We like how Stax has diversified its services to include pre-made and customizable features that can make payment processing easier to manage for larger businesses. It offers an advanced billing management platform for businesses that run high-volume subscriptions, simple payment services integration for independent software vendors (ISVs), and custom embedded payment solutions for businesses using proprietary software.

Please note the figures below are for businesses that use Stax Pay. Contact Stax to learn custom pricing for Stax Bill, Stax Connect, and Stax Processing.

Stax is equipped with a complete range of credit card payment methods. This includes swipe, EMV, and contactless in-person transactions via mobile and in-store POS hardware integration, as well as payment gateway and ecommerce integration for online transactions.

Stax’s payment features support mid-size to high-volume established businesses with level 2 and 3 data processing, credit card surcharging, and cross-border payment services. In addition to the standard business-to-consumer (B2C) payment processing tools, Stax also offers custom embedded payments capability for proprietary business systems and independent software vendors.

Stax provides dispute management features via Stax Connect. It includes alert notifications for initiated and ongoing chargeback disputes and a messaging feature that allows users to respond to chargeback claims and upload supporting documentation to challenge the chargeback.

With Stax, businesses get 24/7 support via phone and email. High-volume clients enrolled in customized payment services are provided with a dedicated account manager. The Stax website includes an extensive knowledge base for every Stax solution and is regularly updated. A live chat tool is also available within the merchant account platform.

Overall Reviewer Score

Average User Review Scores

Why we chose Square

Square is an all-in-one POS solution that includes a built-in payment processing system. Unlike other providers on our list, Square is a payment facilitator, not a traditional merchant account provider. This means businesses are provided with one of Square’s aggregate merchant accounts, which does not require a strict approval process (ideal for new businesses) but is less stable than a dedicated merchant account.

That said, Square provides the best value for new businesses, with minimal startup costs and no monthly fees. It is HIPAA compliant so it is compatible with small healthcare services and offers a CBD program for merchants that sell cannabis products.

Square supports all types of credit card payment methods for both in-person and remote transactions. On top of swipe, EMV, and contactless payments, Square offers in-house buy-now-pay-later services and peer-to-peer (P2P) payments.

With Square, businesses have access to a payment gateway, virtual terminal, invoicing, and recurring billing features. The free mobile app is highly rated and is compatible with iOS and Android devices. Square is also HIPAA compliant, so it can be used by small clinics, pharmacies, and other healthcare services.

One reason Square stands out is its free account with full-featured business management software. Square allows users to sign up for a merchant account, launch a business, and start accepting credit card payments with minimal (even $0) upfront cost.

A free Square account includes:

Aside from the mobile card reader, all of Square’s proprietary POS hardware also comes with a built-in credit card reader. This includes an iPad stand option for businesses that prefer to use their iPads in an in-store setup. Each one can process swipe, EMV, and contactless payments, plus a customer display for tipping, signature capture, and customer feedback collection.

Overall Reviewer Score

Average User Review Scores

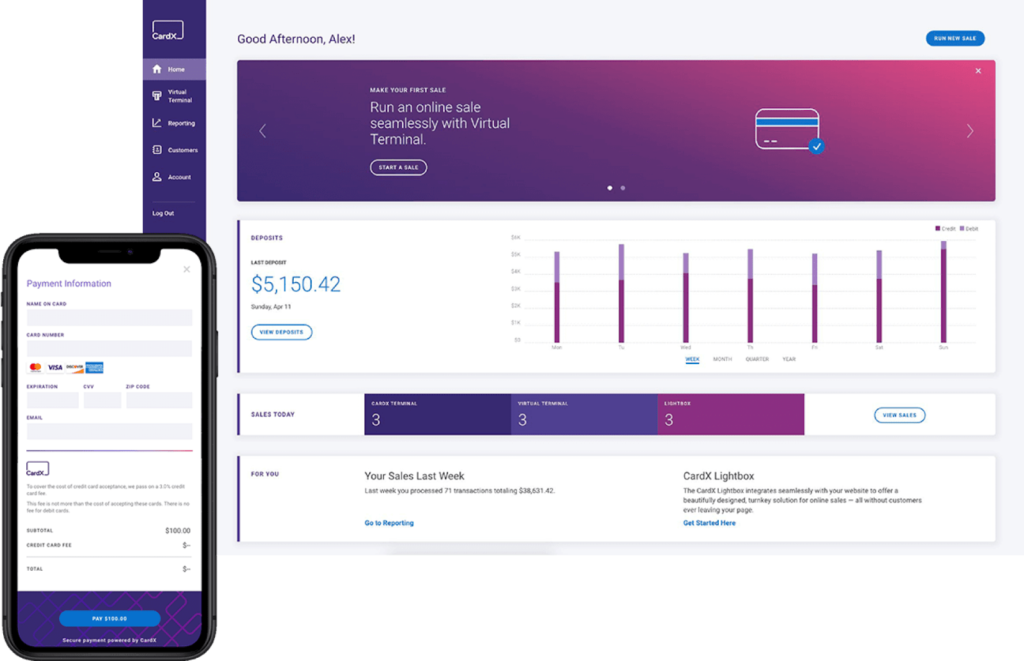

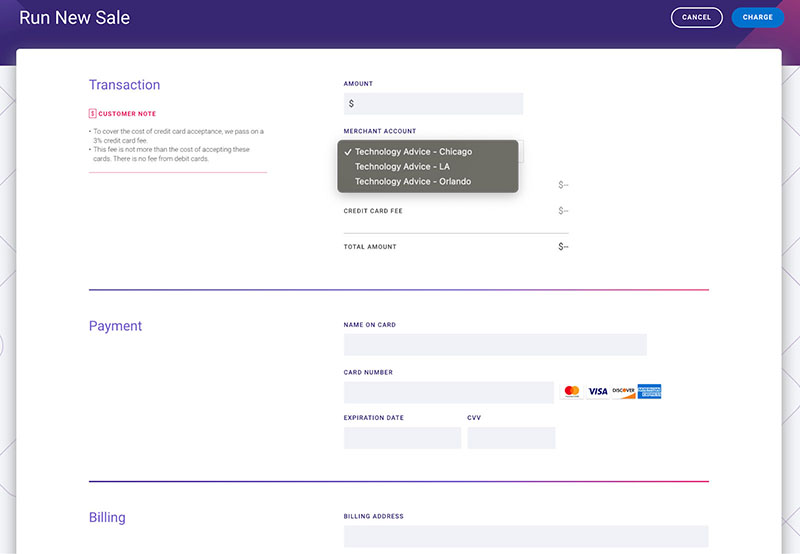

Why we chose CardX

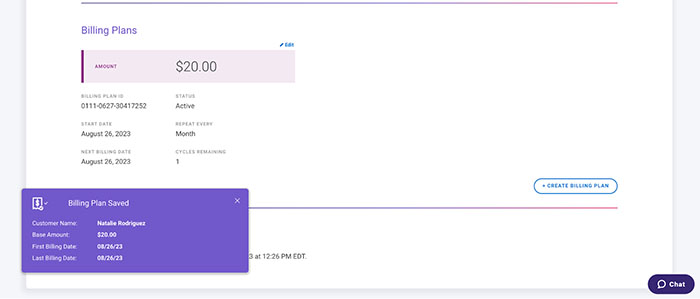

CardX is an expert in surcharging compliance and is Mastercard’s exclusive surcharging partner. It offers surcharging programs for online and in-person transactions. The system is equipped with an invoicing and subscription management feature, as well as a CRM and virtual terminal platform.

We like how CardX doubles down on compliance to provide users with a reliable surcharging program and even conducts free merchant training. CardX also supports simple and advanced online checkout customization via Lightbox. Its subscription management tools are integrated with CardX’s customer profiles, so it’s easy to track and manage accounts receivables. Users have control over fraud protection features such as address verification and CVV settings to match their acceptable risk level.

CardX provides in-person and online credit card payment processing. Debit cards are the preferred alternative payment method. The checkout platform can automatically detect whether a credit or debit card is used.

WIth CardX, users can create and send invoices with embedded checkout forms. It can also create billing templates and track outstanding receivables. A virtual terminal is also available to process manual payments. For online payments, CardX provides Lightbox to create simple and customized online checkouts that can seamlessly integrate with any ecommerce platform.

One of CardX’s outstanding features is its reporting functionality. It provides sales and deposit records that are also integrated with customer profiles. Aside from filtering options, users can also initiate various actions, such as sending payment requests, issuing reminders for outstanding receivables, and viewing complete transaction details.

CardX allows users to collect payments in person. It offers pre-programmed stand-alone card terminals that can also be used alongside POS systems. CardX provides users with the option to purchase the card terminal outright or through a monthly plan. Aside from the mobile card reader, all of Square’s proprietary POS hardware also comes with a built-in credit card reader. This includes an iPad stand option for businesses that prefer to use their iPads in an in-store setup. Each one can process swipe, EMV, and contactless payments, plus a customer display for tipping, signature capture, and customer feedback collection.

Overall Reviewer Score

Average User Review Scores

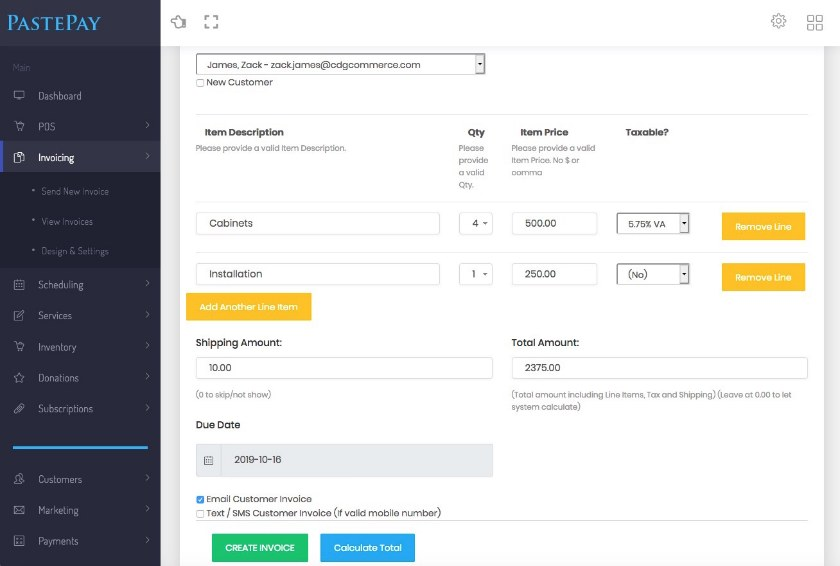

Why we chose CDGCommerce

CDGCommerce is a family-owned merchant account services provider that offers a wide range of credit card processing features and multiple payment gateway integrations. It uses TSYS as its back-end processor and provides in-person and online payment services to businesses of all sizes.

CDGCommerce makes our list as the best choice for growing all business types, including restaurants. This is because the system is compatible with popular restaurant POS systems such as Touchbistro, Lightspeed, and Harbortouch to name a few. It even offers flexible pricing to match any level of sales volume. CDGCommerce also provides top notch chargeback management tools that work best for restaurants that accept online orders.

CDGCommerce supports all types of credit card payment methods. It provides in-person payment processing with card terminals that can process swipe, EMV, and contactless payments. Its online checkout forms can also integrate with popular ecommerce platforms such as BigCommerce and Shopify.

Through its payment gateway integrations, CDGCommerce offers invoicing and virtual terminal solutions. It also supports automated billing and subscription management and mobile payments through the free CDGCommerce mobile POS app.

With CDGCommerce, businesses have access to a number of payment gateway options. Depending on the user’s subscription plan, CDGCommerce may waive fees for Authorize.net and Quantum. Other available payment gateways include NMI, PayPal, and Shopify.

CDGCommerce provides businesses with a chargeback management platform. It allows users to adjust fraud detection settings to match their acceptable risk level. CDGCommerce is equipped with fraud detection tools such as 3D Secure and IP and address verification. In cases where chargeback claims are filed, CDGCommerce will notify and assist in responding to the disputes.

Credit card processing is where businesses accept credit cards as a form of payment in exchange for goods or services. A credit card terminal (for in-person transactions) or an online checkout form (for online transactions) is linked to a payment processor.

Credit card processing happens in a matter of seconds. When a customer uses their credit card to make a payment, the card information is securely transmitted to the customer’s bank that issued the credit card for approval (or rejection).

Payment processors provide businesses with services such as payment gateways, invoicing tools, cross-border payment processing, and level 2 and 3 data processing for B2Bs, to name a few.

Credit card processing fees are made up of interchange rates issued by card networks, fees from the acquiring bank, and markup from the payment processor. There are different structures used by payment processors to assess credit card processing fees:

Consider the following criteria when choosing a credit card processor:

Businesses that want to accept credit card payments should expect credit card transaction fees to account for a significant portion of their operational costs. As such, business owners should know what type of fee structure is best based on sales volume and choose a payment processor that offers flexible pricing. The best credit card processing companies offer flexible fee structures and customized rates.

Credit cards can be used to make payments in a number of ways, and customers all have their own preferred ways to pay. So, the best credit card processing companies can offer a wide range of methods for processing credit card payments. Look for providers that offer both in-person and remote credit card payment methods without extra monthly fees to access these tools.

Not all payment processors offer a complete suite of services. Some providers may not have a built-in virtual terminal, while others may not support level 2 and 3 data processing for B2Bs. At best, identify which type of credit card payment processing service you need and choose a provider that supports these features at no extra cost.

Keeping chargebacks at bay is crucial for businesses to continue accepting credit card payments. Look for payment processors that include chargeback management tools, allowing you to respond promptly to chargeback claims.

Fraud protection and security are top priorities for keeping your business safe from fraudulent transactions. The best credit card processing companies should be able to tell you all the security measures they have in place to protect your data, such as end-to-end encryption, tokenization, and 3D Secure.

Even better if the system provides you with a platform that displays identified suspicious transactions and the ability to manually adjust fraud detection tools.

Cost effectiveness should be the key consideration in choosing the best credit card processor. You should only be paying for features that you need, with a credit card processing fee structure that allows you to maximize your savings.

We find Helcim the most versatile credit card processor because of its fee structure that automatically offers lower rates as your business scales, along with the free software it provides.

Payment Depot and PaymentCloud are the best options for businesses that prefer a customized solution. Both offer custom rates and work with merchants to set up a suite of payment services tailored specifically to their business needs. Choose PaymentCloud if you run a high-risk business and Payment Depot for a standard, low-risk merchant account.

We highly recommend Stax for large-volume and enterprise-level businesses. In addition to wholesale credit card rates, Stax offers a broader range of payment services to accommodate the needs of bigger companies, such as subscription service providers and independent software vendors.

Square is the best choice for new and small businesses. It offers the best value in a forever-free plan that allows businesses with a limited budget to start accepting credit card payments with nearly zero upfront cost.

Those who are looking for a fully compliant surcharging program should consider using CardX. It supports in-person and online surcharging with reasonable volume-based monthly fees.

Lastly, but not least, choose CDGCommerce if you want a payment processor that can scale with your business from the ground up. It offers flexible volume-based plans ideal for small, mid-size, and large businesses. CDGCommerce integrates with a number of restaurant POS systems, making it ideal for businesses in the food industry.

The best credit card processing service should provide you with payment processing tools that match your business needs while also offering a fee structure that can maximize your savings.

In-person payment methods are the best when accepting credit card payments. This is because the transaction fees are significantly lower and the risk of chargeback claims is less compared to online and other remote payment methods.

A good credit card processing rate depends on your business’s sales volume. New and small businesses that only process $10,000 in credit card sales per month can use flat rate pricing that’s easy to understand. Growing and large volume businesses will benefit more from interchange plus rates and wholesale subscription, respectively, because the increase in credit card sales volume produces more discounts.